Quick Navigation

Report Overview

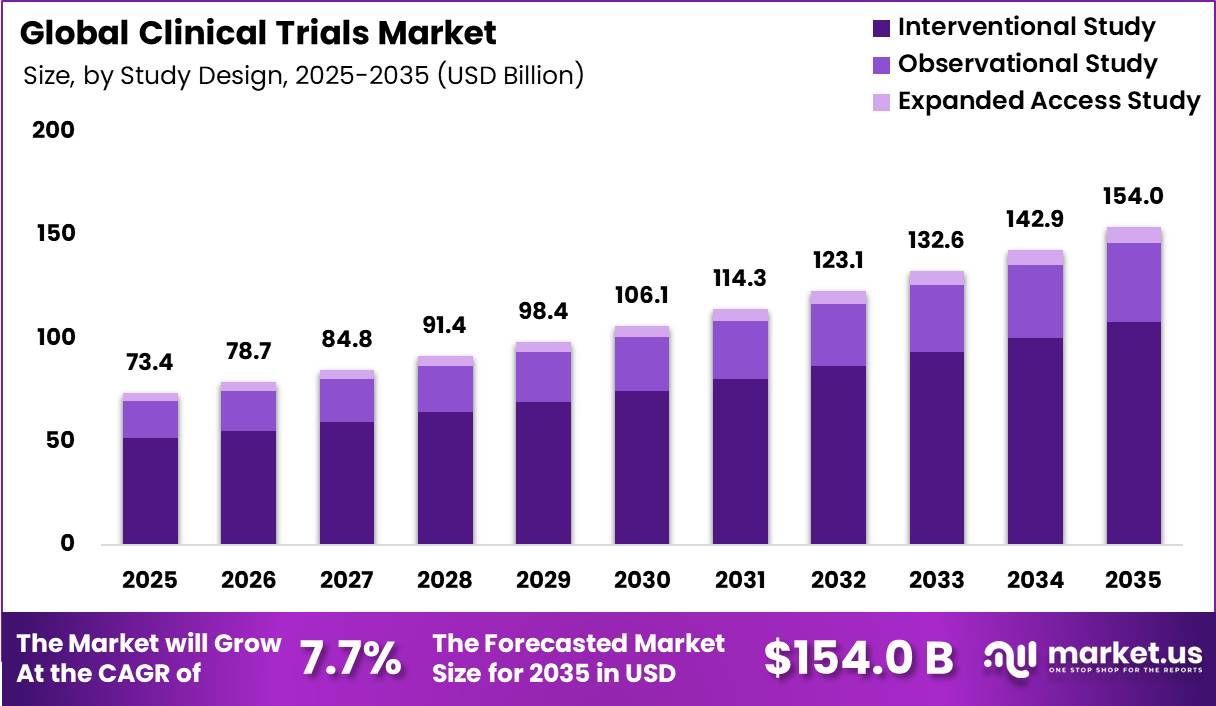

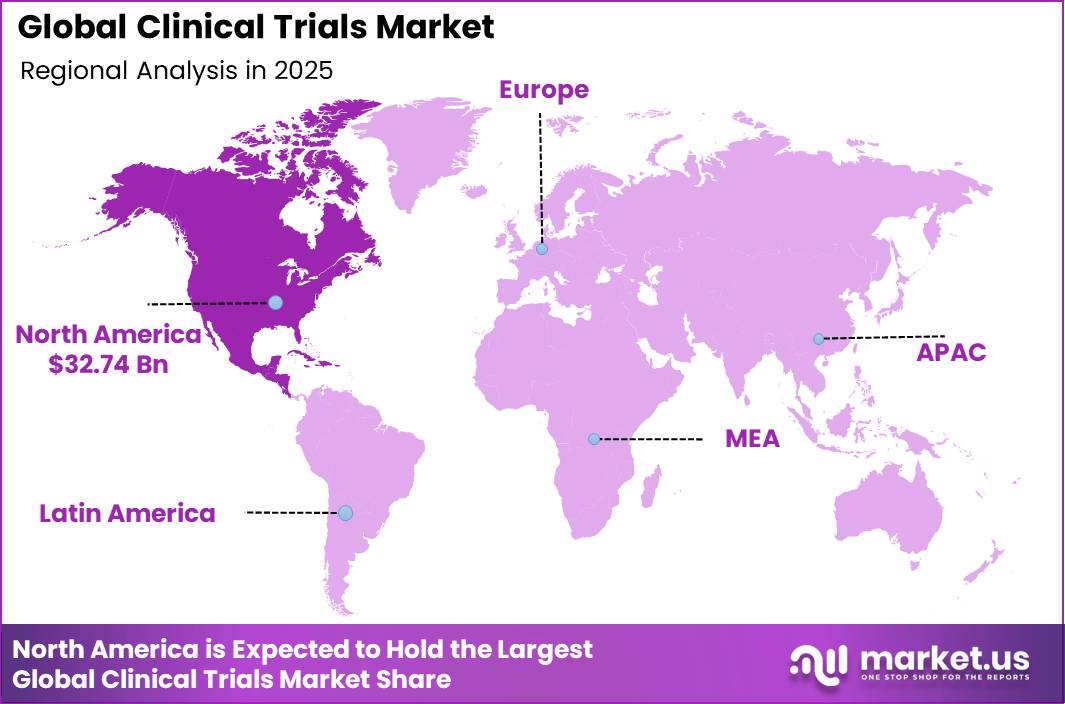

Global Clinical Trials Market size is expected to be worth around USD 154.0 Billion by 2035 from USD 73.4 Billion in 2025, growing at a CAGR of 7.7% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 44.6% share with a revenue of US$ 32.74 Billion.

The clinical trials market forms a vital foundation within healthcare and pharmaceutical supply chains, ensuring safe, effective drug testing and regulatory compliance before new therapies reach patients. Market demand is driven directly by expanding research pipelines, rising global life expectancy, and a higher burden of chronic illnesses. Pharmaceutical and biotech developers remain the primary buyers, using advanced clinical software, integrated databases, and third-party vendor networks to shorten development timelines.

Allocation of capital depends very much on the stage at which the clinical trials are being conducted. Phase III clinical trials call for the most extensive capital expenditure since they deal with large international patient populations. The subsequent stages of R&D follow in sequence, beginning with early-phase safety trials, mid-phase safety studies, and post-market studies.

The stringent regulatory guidelines on clinical evidence from controlled clinical trials influence the approaches to designing such trials. Interventional designs thus occupy the bulk of the market share, while the remaining market is captured by observational trials and compassionate use programs.

There is an increasing trend towards decentralization in trial designs as well as using remote monitoring and AI-enabled data management to handle the complexity of therapy data. The areas of oncology, cardiology, neurodegenerative conditions, infections, and metabolism remain dominant.

North America continues to be the dominant regional market due to existing infrastructure and concentrated drug developers, whereas Europe follows closely behind because of its stable regulatory environment. The Asia Pacific region serves as a rapidly growing area owing to the large number of patients, whereas Latin America and the Middle East regions are still developing their own execution capabilities. Developers depend greatly on outsourcing services for managing such a wide geographic presence.

Key Takeaways

- Market Size: The market size of global clinical trials was evaluated at USD 73.4 Billion in 2025, and it is estimated to expand up to USD 154.0 Billion by 2035.

- The market is expected to witness a CAGR of 7.7% during the forecast period.

- Phase Type Analysis: Phase III trials accounted for the largest market share of 49.8% in 2025.

- Study Design Analysis: Interventional Studies accounted for the largest market share of 70.3% in 2025.

- Indication Analysis: Oncology accounted for the largest market share of 30.2% in 2025.

- Service Type Analysis: Outsourcing Services accounted for the largest market share of 67.3% in 2025.

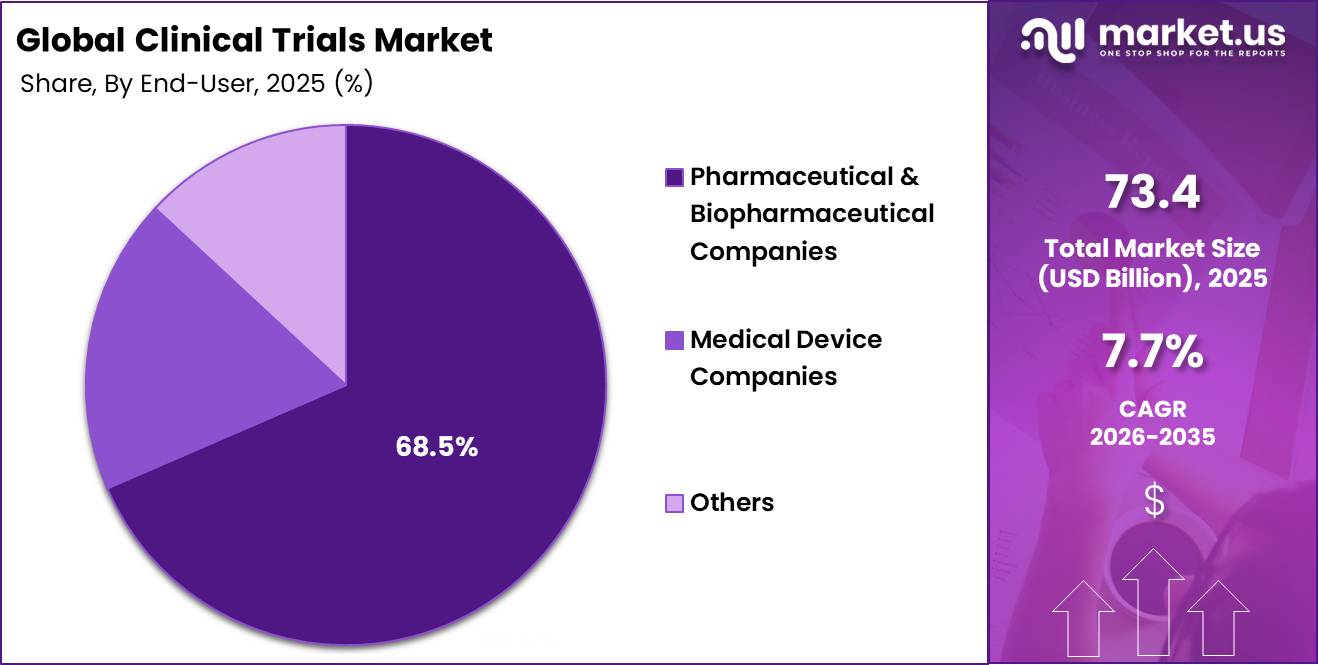

- End User Analysis: Pharmaceutical & Biopharm accounted for the largest market share of 68.5% in 2025.

- Regional Analysis: In 2025, North America leads the way with 44.6% share in the global market, owing to the well-established infrastructure in the region.

Phase Analysis

Phase III trials lead market revenue through large-scale validation requirements.

The Phase III trials segment is the largest part of the market, holding a 49.8% share because of strict rules that require human testing to prove a drug’s effectiveness and safety before it can be approved. However, the growth of this segment largely depends on how many patients are willing to participate and the costs involved in keeping them engaged.

Phase I clinical trials will continue to be the fastest-growing segment due to an inflow of innovative drugs in terms of biologics, cells, and genes. The rapid growth of this segment will be largely attributed to investment from biotechnology and regulatory acceptance of adaptive study designs for fast human safety assessments.

The most promising and upcoming segment will be Phase IV post-marketing surveillance trials, since there has been increasing pressure from health organizations around the world to provide long-term evidence regarding the efficacy and safety of the drug before it can be approved. Growth will be directly dependent on digital technologies and wearables.

Study Analysis

Interventional studies dominate trial design via rigorous regulatory standards.

The Interventional Study segment is the dominant market, commanding a 70.3% segment share due to government rules that require testing on real people to make sure drugs are safe. However, how much this segment grows depends a lot on how easily patients can be found, the need to prove that treatments work, and the high cost of getting medications.

Observational studies are the fastest-growing category. The rapid growth of observational studies is due to the increasing number of health organizations relying on real-world evidence and long-term observation to confirm safety. Growth drivers include the development of electronic health records, digital healthcare registries, and post-market monitoring compliance regulations.

Expanded access studies are the leading upcoming category and are projected to experience continuous growth. The reason for the trend is that patients suffering from life-threatening diseases require access to investigational drugs prior to approval. Growth drivers include compassionate use program policy changes, patient monitoring portals, and drug allocation from pharmaceutical companies.

Indication Type Analysis

Oncology remains the leading indication driven by high global disease burden.

The Oncology segment is the dominant market, commanding a 30.2% segment share due to many companies pouring their efforts into research and development to cure complex tumor. Growth is attributed to increasing R&D pipelines, increasing cancer incidences, and fast-tracking drug approval processes from health agencies.

The metabolic disorder is one of the quickest growing segments. The rapid growth is as a result of increasing global demand for next generation obesity treatments, life-style diseases and diabetes therapies. Patient demands, changing company investments, and increased public awareness have a great effect on the growth.

CNS disorders can be considered a huge future therapeutic segment. This is due to the need to find new treatment for age-related neurological conditions like Alzheimer’s among others as a result of the aging world population. Growth in this sector has been fueled by advances in neuro-imaging technology, high funding from the government, and positive regulations for rare diseases.

Service Type Analysis

Outsourcing services thrive as sponsors leverage specialized CRO.

The Outsourcing Service segment is the dominant market, commanding a 67.3% segment share due to a high dependence of pharmaceutical companies on the use of Contract Research Organizations (CROs) in managing various aspects of conducting studies. Outsourcing becomes the key way of handling clinical trials as it is not feasible to handle large volumes of global data flow within an organization. The development factors include cost reduction needs, shortened timelines, and expertise of worldwide specialists.

Functional service providers (FSP) outsourced solutions have been gaining popularity at a rapid pace recently. It is explained by the willingness of firms to delegate only certain functions of the trial process to outside experts, such as data management or writing. The development of this field is greatly dependent on flexibility, potential cost savings, and specific data management demands.

The fully decentralized trial outsourcing market is expected to become the fastest-growing segment in the near future. It will be caused by a change in the traditional approach to conducting trials when companies switch to virtual or hybrid studies in order to maintain patients’ involvement in the research process. This field is growing because of the emergence of telemedicine technologies and special software.

End User Analysis

Pharmaceutical companies maintain leadership through extensive R&D pipelines.

The Pharmaceutical & Biopharm segment is the dominant market, commanding a 68.5% segment share due to their significant corporate capital networks and wide drug pipelines, which need vast experimentation. The major drivers of this segment are the high expenditure on the manufacturing and development of biological products, biosimilar products, and highly specified treatments.

Factors influencing the domination of this segment include the enormous budgets of companies dedicated to research and development, high disease burden, and constant innovations aimed at bringing new products to the market.

Medical Devices come second among fast-growing segments. Their fast growth comes from changes in the global medical policies, which now require more direct human data rather than lab evidence before granting any company marketing permission. The factors that have contributed significantly to this growth include rapid development of the next generation of surgical technology, digital medical devices, cardiac implant devices, and changing regulatory policy.

Research Institutes and Academic Institutions are one of the fast-upcoming sectors with steady growth prospects. This has come about because government health authorities and universities are now funding initial and investigative studies. The main areas of growth include public-private partnerships, increased national health grants, and focus on designing target orphan drugs for rare diseases.

Key Market Segments

By Phase Type

- Phase I

- Phase II

- Phase III

- Phase IV

By Study Design

- Interventional Study

- Observational Study

- Expanded Access Study

By Indication

- Oncology

- Cardiology

- CNS Disorder

- Infectious Disease

- Metabolic Disorder

- Renal/Nephrology

- Others

By Service Type

- Outsourcing Service

- In-House Service

By End User

- Pharmaceutical & Biopharmaceutical Companies

- Medical Device Companies

- Others

Driver

Risk based GCP modernization and protocol flexibility

The 2025 finalization of ICH E6(R3) by FDA materially improves the commercial viability of more adaptive, technology enabled, and proportionate trial operating models because it explicitly supports flexible designs, broader data sources, quality by design, and risk based quality management.

For sponsors, that shifts spend away from blanket on site monitoring and overly rigid documentation toward targeted oversight, central monitoring, and protocol architectures built around critical to quality factors, which typically improves cycle efficiency in trial start up, amendment handling, and deviation management.

The practical market effect in 2026 is not just compliance work; it is increased willingness to launch more complex global studies and hybrid protocols because regulatory expectations now better align with decentralized workflows, digital data capture, and differentiated risk controls.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk-based GCP modernization and protocol flexibility | +1.6% | North America core, EU, Japan, ICH-aligned APAC | Short term (≤ 2 years) |

| EU CTIS harmonization and cross-border trial activation | +1.3% | EU core, EEA, UK spill-over, CEE hubs | Short term (≤ 2 years) |

| Decentralized and digital endpoint adoption | +1.8% | North America core, EU, APAC urban corridors | Medium term (2-4 years) |

| Oncology and precision medicine pipeline intensity | +2.1% | US core, EU5, Japan, South Korea, China selective | Medium term (2-4 years) |

| Public-sector translational funding and network expansion | +1.1% | US core, EU programs, selected APAC research clusters | Medium term (2-4 years) |

| AI-enabled recruitment, monitoring, and data operations | +1.4% | North America core, EU, India service hubs, APAC | Medium term (2-4 years) |

Challenge

Cross Border Compliance Load

The regulatory environment is not freezing clinical trials in 2026, but it is materially raising operating friction as sponsors manage overlapping expectations on CTIS transition in Europe, decentralized trial controls, data governance, and diversity planning across jurisdictions; EMA requires ongoing legacy trials to comply with the Clinical Trials Regulation and be recorded in CTIS from 31 January 2025, while the FDA’s recent guidance environment adds more detailed expectations around decentralized elements and diversity action planning.

That compliance layering supports an estimated 0.9% point CAGR drag because multinational studies now face more synchronized document management, localized legal review, country specific SOP adjustments, and higher submission rework, with realistic execution penalties of 20 to 45 extra days in cross border startup, 8% to 12% more regulatory operations spend per pivotal study, and more frequent midstream process corrections when digital, consent, or enrollment equity assumptions fail local interpretation.

The strategic response is a shift from country by country compliance management to modular global operating architecture, including reusable dossier components, jurisdiction specific regulatory playbooks, embedded privacy engineering, and earlier comparator country sequencing, because firms that continue treating compliance as an end stage submission task will preserve booked revenue but underperform on timing, margin, and portfolio velocity.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Site Workforce Deficit | -1.3% | North America core, EU site networks, APAC metro hubs | Medium term (2-4 years) |

| Protocol Complexity Creep | -1.1% | Global multisite studies, North America core, EU regulatory hubs | Medium term (2-4 years) |

| Cross-Border Compliance Load | -0.9% | EU regulatory hubs, North America, Japan, multi-country programs | Medium term (2-4 years) |

| DCT Integration Instability | -0.8% | North America, Western Europe, advanced APAC markets | Short term (≤ 2 years) |

| LMIC Capacity Imbalance | -0.7% | LATAM growth corridors, South Asia, Africa, global enrollment programs | Long term (≥ 4 years) |

| Cybersecurity Vendor Exposure | -0.6% | North America core, EU data zones, global eClinical ecosystems | Medium term (2-4 years) |

Restraints

Escalating trial cost inflation

Escalating clinical trial costs are increasingly eroding sponsor economics, with Phase III budgets rising ~25–35% since 2018 and now averaging in the mid-$30M range per program (2024–2025). The main drivers include more complex protocols, higher pass-through vendor costs, inflation in site labor, and expanded data requirements (over 200% increase in Phase III data collection over the past decade).

Protocol amendments (typically 3–4 per trial) add 2–3 months and ~3–5% extra cost each.Additional pressures include mid-single-digit annual wage growth in the US/EU, 8–10% increases in logistics and cold-chain costs for advanced therapies, and growing use of digital tools (eCOA, eConsent, wearables), which now account for ~10–15% of late-stage trial budgets.

Overall, this cost inflation is compressing pharma IRRs by an estimated 150–250 bps, leading to fewer marginal Phase II starts and more selective pipeline investment. For mid-cap biotech, where a single Phase IIb/III program can consume 60–80% of R&D budgets, unexpected 20–25% overruns often trigger dilutive fundraising, partnering deals, or reduced site footprints, delaying readouts by 6–12 months.

At the industry level, these dynamics create an estimated ~2 percentage point drag on clinical trial market CAGR as sponsors delay programs, renegotiate CRO contracts, and avoid higher-cost geographies.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating trial cost inflation | -2.2% | North America core, EU, Japan | Short–Medium term |

| Regulatory tightening and transparency mandates | -1.6% | US, EU, UK, global multicentre | Medium–Long term |

| Patient recruitment and retention bottlenecks | -1.9% | North America, EU, APAC corridors | Short–Medium term |

| Data complexity, interoperability, and quality risks | -1.4% | Global, especially multi-region Phase II/III | Medium–Long term |

| Site capacity, workforce, and CRO execution constraints | -1.7% | North America core, EU, India, China | Short–Medium term |

| Geopolitical, supply chain, and localization frictions | -1.3% | CEE, China, Middle East, LatAm | Medium–Long term |

Opportunity

Hybrid rare disease enrollment hubs

Rare disease clinical trial infrastructure continues to be largely concentrated within fragmented tertiary academic centers, limiting scalability and consistent patient access. In the current baseline model, operational inefficiencies are commonly observed due to geographically dispersed patient populations, low disease prevalence, and dependence on site-centric recruitment processes. As a result, screening yield remains constrained, and significant portions of eligible patients are not systematically captured within existing recruitment frameworks.

The future growth trajectory is being shaped by the development of cross-border hybrid enrollment hubs that integrate genomic pre-screening, remote consent mechanisms, decentralized laboratory collection networks, travel coordination support, and home-based follow-up services. This model enables conversion of currently under-penetrated rare disease and orphan populations into a more structured and scalable service architecture. In rare oncology, for instance, approximately 25% of adult malignancies in selected trial datasets are represented by rare cancer subtypes, highlighting the expanding relevance of molecular stratification in unlocking clinically meaningful patient pools that were previously operationally inaccessible.

Evidence suggests that integrated patient registry linkages, advocacy network collaboration, and hub-and-spoke teletrial frameworks could materially improve trial efficiency and enrollment performance. Potential gains include a 20%–30% increase in referral conversion, a 12%–18% reduction in screen failure rates, and an 8%–12% improvement in patient retention. On a global scale, the emergence of an orchestration layer for decentralized enrollment is projected to generate incremental value in the range of USD 3–5 billion by the early 2030s, particularly across oncology, neurology, and pediatric therapeutic areas where traditional site-centric models continue to underutilize addressable patient populations.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| LMIC site-network buildout | +2.1% | APAC, Africa, LatAm, Middle East | Medium term (2-4 years) |

| Hybrid rare-disease enrollment hubs | +1.8% | North America, EU, Japan, GCC | Short term (≤ 2 years) |

| AI protocol-to-patient matching | +1.6% | North America core, EU, China, India | Short term (≤ 2 years) |

| Cell and gene trial enablement platforms | +2.4% | US, EU, Japan, South Korea | Medium term (2-4 years) |

| Siteless post-approval evidence models | +1.4% | US, EU, UK, Australia | Medium term (2-4 years) |

| Sponsor roll-up of specialty CRO micro-capabilities | +1.9% | US, EU, India, Singapore | Long term (≥ 4 years) |

Regional Analysis

North America dominates the global clinical trials market during the forecast period.

The North American region was estimated to be worth a market share of 44.6% in 2025, and is expected to continue dominating the global market until 2035. The continued dominance is attributed to the quick adoption of cutting-edge technologies such as artificial intelligence and decentralized trial platforms within the field of clinical research. Top firms including IQVIA, Labcorp, and ICON plc are rapidly expanding their presence in the region through the provision of virtual solutions and remote monitoring in several trial phases.

In addition, the market is supported by large investments in research and development, along with a well-established healthcare system that can carry out complex Phase III trials, which account for the biggest portion of global revenue. Also, there is strong demand in the United States because of favorable government policies and a regulatory environment that encourages innovation in specialized areas like oncology.

Looking ahead, the APAC region is expected to grow the fastest, thanks to a rapidly increasing compound annual growth rate. The reason for the quick growth in the market is attributed to the availability of large pools of untapped patients, making the process of enrolling participants easier and reducing costs associated with operations in comparison to Western countries.

The clinical trial landscape is changing, with more global companies focusing on Asia. They are increasingly looking to countries like India, China, and South Korea to reduce their reliance on Western markets. This shift is driven by the large number of patients who haven’t received previous treatments, which helps speed up the process of finding participants.

Also, these regions have many specialized contract research organizations that provide reliable data at a lower cost. To protect against possible problems related to logistics and politics, companies are using a strategy called “China Plus One.” This lets them stay strong in China’s big market while also setting up trials in India and South Korea to improve efficiency and reduce risks from regulations.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Nordic Countries

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

IQVIA and ICON plc Expanded Digital Clinical Suites to Accelerate Decentralized Trial Execution and AI-Driven Patient Recruitment. Also, Fortrea and Medpace Launched Advanced Analytics Platforms to Increase the Efficiency of Global Phase III Trials.

The global clinical trial market is characterized by fierce competition, with market leaders being determined on the basis of large mergers and acquisitions in addition to integration of digital health solutions. Examples of some companies that have become leaders of the global clinical trials industry include IQVIA Inc., ICON plc, LabCorp, Thermo Fisher Scientific (PPD), and Parexel.

Adoption of new technological innovations including artificial intelligence and digital tools is the main determinant of competition in the market. Leading players usually make high-value mergers and acquisitions and develop integrated eClinical solutions to strengthen their market positions.

In June 2023, IQVIA improved its services by upgrading its AI-driven “One Home” platform to make managing decentralized clinical trials more efficient and better collect geographic data. This move helped expand outsourcing options, giving sponsors digital tools to speed up trial processes and lower costs.

Around the same time, in early 2024, Fortrea and Medpace launched specialized site support services focused on boosting patient recruitment for challenging oncology and rare disease studies, which in turn helps improve the efficiency of phase III trials.

Major Key Players

- Novartis AG

- Pfizer Inc.

- ICON plc

- Cadiya (Clinipace)

- Merck Sharp & Dohme LLC

- Charles River Laboratories

- Medpace

- Parexel International Corporation

- Pharmaceutical Product Development (Thermo Fisher Scientific)

- Qserve

- SGS SA

- Syneos Health

- The Emmes Company

- Veeda

- Worldwide Clinical Trials

- Other Key Players

Key Development

- Novartis AG (Oct, 2025) : Novartis agreed to acquire Avidity Biosciences for approximately USD 12 billion, strengthening its neuromuscular and RNA-based clinical pipeline. The deal includes late-stage clinical assets targeting rare muscle disorders and is expected to close in 1H 2026 after structural separation of SpinCo.

- Pfizer Inc.(Nov, 2025): Pfizer intensified its competitive position in metabolic disease trials through a bidding expansion for Metsera, with deal valuation reaching nearly USD 10 billion. The development reflects aggressive pipeline expansion in obesity-related clinical programs.

- Merck Sharp & Dohme LLC (Nov, 2025): Merck entered a strategic funding agreement of USD 700 million with Blackstone Life Sciences to support late-stage oncology clinical trials of sac-TMT, an antibody-drug conjugate being evaluated across multiple tumor types in Phase II–III programs.

- Mallinckrodt & Endo International (Mar, 2025): Both companies announced a USD 6.7 billion merger, forming a combined entity with expanded capabilities in generics and branded drug clinical development, aiming to improve pipeline efficiency and long-term trial investment capacity.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 73.4 Bn |

| Forecast Revenue (2035) | US$ 154.0 Bn |

| CAGR (2026-2035) | 7.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Phase Type (Phase I, Phase II, Phase III, Phase IV), By Study Design (Interventional Study, Observational Study, Expanded Access Study), By Indication (Oncology, Cardiology, CNS Disorder, Infectious Disease, Metabolic Disorder, Renal/Nephrology, Others), By Service Type ( Outsourcing Service, In-House Service), By End User (Pharmaceutical & Biopharmaceutical Companies, Medical Device Companies, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Novartis AG, Pfizer Inc., ICON plc, Cadiya (Clinipace), Merck Sharp & Dohme LLC, Charles River Laboratories, Medpace, Parexel International Corporation, Pharmaceutical Product Development (Thermo Fisher Scientific), Qserve, SGS SA, Syneos Health, The Emmes Company, Veeda, Worldwide Clinical Trials, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |